How the U.S. Federal Debt Burden Impacts Your Personal Finances

Raising Inflation and Potentially Using Cryptocurrency as Methods for Debt Reduction

This week’s subject might seem a bit “off course”, but from a personal finance perspective, it is important to understand the world we are living in and what we may see in the future. The United States isn’t great at managing its own finances and is in desperate need of a course or ten on Conquering Personal Finance. As long as lawmakers, notably the US Congress and Executive Branch, are in charge of our tax dollars the outcome looks bleak. As you plan your own budget, and perhaps weigh where to place your investment opportunities, knowing the landscape around you will help you make better decisions.

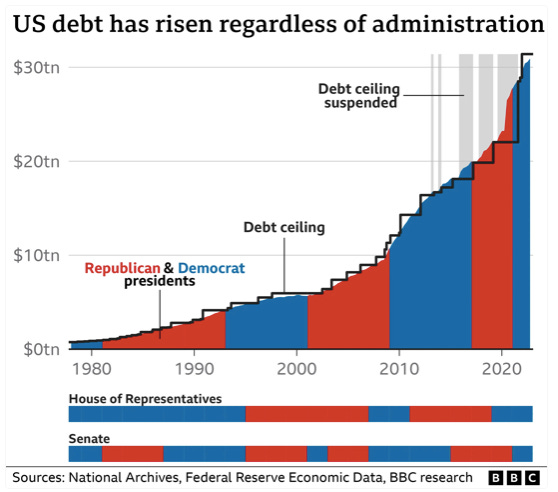

The United States, like many nations, has long grappled with a towering federal debt burden that raises concerns about economic stability, fiscal sustainability, and the long-term health of its financial institutions. As of today, the national debt exceeds $36 trillion (and rising), a figure that continues to climb amidst debates over government spending, taxation, and monetary policy. While traditional methods such as austerity measures (DOGE), tax increases, and cuts to public spending have been attempted with mixed results, there are growing discussions about unconventional solutions, including leveraging inflation and creating a government-backed cryptocurrency to address this monumental challenge.

Inflation refers to the rise in the general level of prices for goods and services over time. It reduces the purchasing power of money (US Dollars), meaning that each of your dollars buys fewer goods and services. For governments holding large debts, inflation can be a double-edged sword—it devalues the real value of debt, but it can also create economic distortions for its citizens if not managed carefully. Remember when our leaders were patting us on the head and telling us not to worry about “transitory” (temporary) inflation?

When inflation rises, the nominal (existing) value of debt remains constant, but its real value decreases. For example, the $36 trillion owed by the U.S. government today would be worth significantly less in real terms if annual inflation were to increase to, say, 5%-10%. This effectively makes debt cheaper to repay, as long as government revenues, typically collected through taxes, rise in tandem with inflation. In our world today, inflation is the primarily the result of printing about ten years’ worth of money in about two years’ time during and in the aftermath of the global pandemic.

The U.S. government has some control over inflation through monetary policy tools managed by the Federal Reserve, such as adjusting interest rates or employing quantitative easing (printing more money). Printing money would be a great tool for us all if we had the power, but it essentially makes the US government the casino house. As we all know, house rules always favor the casino, and when they don’t, the rules change. By aiming for a controlled rise in inflation, policymakers devalued debt and teetered with runaway inflation that could potentially destabilize the economy. Realistically, it is still too early to tell the end result. Remember the housing crisis from 2008? That is still washing out seventeen years later. These moves take time to resolve themselves.

Inflation has been used historically to manage debt burdens. For instance, after World War II, many nations, including the United States experienced significant inflation, which eroded the real value of wartime debts. Though the post-war period was marked by economic growth that contributed to debt reduction, inflation played a key role in lightening the fiscal load. However, relying solely on inflation as a tool for debt management carries risks. High inflation can lead to reduced consumer purchasing power, higher interest rates, and loss of confidence in the home currency. Inflation can cripple consumers (us) and cause us to stop buying things, or worse, borrow to buy. Any widescale strategy involving inflation must be carefully calculated and implemented in conjunction with other economic measures.

Cryptocurrencies, such as Bitcoin and Ethereum, have been introduced to the financial landscape with investing pros offering decentralized, blockchain-based “currency” or “assets” for transactions and value storage. Whether you personally believe in the value of Crypto is your personal choice. However, the potential for a government-backed cryptocurrency as a tool for addressing federal debt is likely going to be an option at some point. The U.S. could introduce a nationally endorsed cryptocurrency—let’s call it “FedCoin”—as a digital “asset” designed to pay off portions of the federal debt. Unlike existing cryptocurrencies, FedCoin would be centrally managed and tied to the value of the dollar, ensuring stability and greater trust among users. By combining innovative blockchain technology with traditional monetary structures, the government could leverage FedCoin to reduce debt dramatically. It’s anyone’s guess what would happen to pre-existing cryptos like Bitcoin, it could be an all or nothing proposition.

PROS

Some of the possible advantages of a “FedCoin” include:

Transparency: Blockchain technology ensures that all transactions are publicly recorded and verifiable, with the possibility associated with the risks of fraud and corruption. Artificial intelligence (AI) based tools should help here.

Efficiency: Digital transactions are faster and often cheaper than traditional payment methods, making debt repayments more streamlined in comparison to large banks and institutions.

Modernization: Introducing a cryptocurrency would position the U.S. as a leader in the global digital economy (whether you believe in it or not), enhancing its economic and technological competitiveness.

HOW WOULD IT WORK?

“FedCoin” could function in several ways to alleviate the debt burden:

Direct Debt Payment: The government could issue FedCoin to creditors, gradually replacing traditional bonds with digital assets (assumes the creditors will accept this as payment).

Economic Stimulation: FedCoin could be distributed to taxpayers or businesses, boosting economic activity and increasing tax revenues, which could then be used to pay down debt.

Global Adoption: If a US backed FedCoin gains international acceptance, foreign governments and institutions could use it for transactions, creating additional revenue streams for the U.S.

· Note: Parking cash, which we take for granted in the US, is not a reality in many parts of the world. Crypto is hard to capture for many foreign governments (for now).

WHAT ARE THE RISKS?

While the idea of a cryptocurrency to manage federal debt is a possible avenue, it comes with its own set of serious risks and challenges:

Maintaining trust in FedCoin would require strong regulatory oversight and technological security. More spending authority in the hands of our lawmakers, what could go wrong?

Cryptocurrency valuations are already volatile, potentially complicating debt repayment.

Opposition from traditional financial institutions and global markets wary of such a shift; they will push back hard. Lobbyists and your representatives will make a lot of money.

If the US government is the ultimate sucker, who is left to buy?

COULD THE U.S. ACTUALLY IMPLEMENT CRYPTO TO REDUCE ITS DEBT?

By combining the controlled introduction of inflation with the implementation of a government-backed cryptocurrency, the U.S. could create a strategy to reduce its debt. Inflation would decrease the real value of the debt, while “FedCoin” could provide a modern mechanism for repayment and economic growth (real or imagined or pencil whipped).

The implementation of this combined strategy would require:

Policy Coordination: Collaboration between the Federal Reserve, Treasury, and Congress to align monetary and fiscal policies. How is that gone in the past?

Digital Infrastructure: Developing a secure blockchain platform for FedCoin and ensuring widespread accessibility and adoption.

Public Engagement: Educating citizens and businesses about the benefits and uses of FedCoin to foster trust and participation.

Figuring out what to do with existing Cryptos.

If executed effectively, the combined strategy could:

Significantly reduce the nominal and real value of the federal debt. It would be a historic coup that would produce a few winners and many losers.

Economic growth through the adoption of cryptocurrency technologies.

Enhance the U.S. position as a global leader in cryptocurrency.

The United States faces a daunting challenge in managing its federal debt, but unconventional solutions such as controlled inflation and the creation of a government-backed cryptocurrency offer tantalizing choices with a variety of outcomes — some good, some disastrous. By combining these approaches, policymakers could tackle the debt burden while modernizing the economy and embracing technological innovation.

Should we all run out and buy a bunch of Crypto? Truthfully, the author has never been a fan and has relied on financial wisdom of the likes of Warren Buffett or JP Morgan’s CEO, Jamie Dimon, when it comes to “funny money”. These views, in fact, could be wrong as long as there is a “greater fool” who comes knocking whether it is crypto, baseball cards or beanie babies. Could the US create a currency out of thin air and use it to knock down existing debt? Absolutely. Will the US create a currency, and like a drunken sailor (or congressman) who finds an unopen bottle, keep drinking? What do you think?

Disclaimer: The author is independent, does not maintain any affiliations with any financial institutions, is not a Certified Financial Planner (CFP) and does not hold any designation as a registered financial advisor. The information provided in this newsletter is for informational purposes only and is provided as a commonsense approach based on real life experiences. Any actions you take based on the information in this newsletter are your responsibility.